The “build it, and they will come” era of self-storage is over. Today, the sector is dominated by institutional capital and data-driven operators, making operational efficiency the primary driver of asset value. In this competitive market, the quality of your management strategy is the difference between a stagnant asset and one that consistently outperforms market cap rates.

3rd-party self-storage management has evolved from simple staffing to a holistic operational strategy. For independent operators and private equity firms, outsourcing to a professional firm has become both a convenient and strategic move to access institutional-grade platforms, sophisticated revenue management, and scalable infrastructure that drives Net Operating Income (NOI).

Key Takeaways:

The decision to hire a self-storage 3rd party management firm is often triggered by a specific lifecycle event or pain point.

Filling a brand-new facility (going from 0% to 85% occupancy) is a cash-flow-negative sprint. It requires aggressive marketing and dynamic pricing that shifts weekly to capture market share. Operators hire professionals to shorten this “lease-up” timeline and reduce the carry cost of the development loan.

A successful operator in Texas may struggle to manage a new acquisition in Colorado due to a lack of local vendors and knowledge of local lien laws. Third-party managers provide instant infrastructure in new markets, ensuring compliance and operational continuity without the operator needing to build a local team from scratch.

Many operators reach a point where their manual spreadsheets and legacy software become ineffective. When a portfolio grows from 3 to 10 sites, the complexity compounds. Third-party managers bring enterprise software stacks—like Monument—that are built for scale, preventing operational bottlenecks.

Building a call center, a marketing department, and an accounting team is expensive. Outsourcing allows an operator to rent this centralized infrastructure for a management fee (the industry standard is typically 5-7% of Gross Revenue) rather than building it with the associated massive overhead.

Private equity firms often buy “mom-and-pop” facilities to roll them into a portfolio. These assets usually have messy data and no systems. A third-party manager can “onboard” these chaotic assets into a unified system in 30-60 days, instantly stabilizing the portfolio and ensuring rapid operational alignment.

For third-party self-storage management companies, technology is no longer an internal efficiency tool—it is the core product being sold to operators. The distinction between a “management firm” and a “technology platform” has effectively collapsed. Operators are not hiring headcount; they are hiring a scalable operating system. As a result, third-party managers competing on legacy, facility-centric software are structurally disadvantaged against firms built on cloud-native, portfolio-first platforms.

Today’s operators evaluate third-party managers through a technology lens first. They assess whether a manager can deliver institutional-grade revenue management, execute ECRI programs with precision, operate hybrid or unmanned facilities through automation, produce real-time, GAAP-compliant reporting, and integrate seamlessly with best-in-class vendor ecosystems. These capabilities are no longer “nice to have”—they are table stakes for winning and retaining management contracts in a capital-constrained, margin-sensitive environment.

This technology directly determines a third-party manager’s cost structure and scalability. Labor remains the largest controllable expense in self-storage operations, and the difference between a legacy stack and an enterprise-grade platform is measurable. A technology-enabled third-party manager can operate a facility at approximately 1.5 full-time employees (FTEs), versus 2.5 FTEs under traditional management models. That delta compounds across a portfolio, flowing directly into higher NOI for operators—and higher margin, more defensible economics for the management company itself.

Not all operator relationships are structured the same way, and for third-party self-storage management companies, this distinction is critical. The level of involvement an operator expects—ranging from fully delegated control to hands-on oversight—directly impacts how a management firm must operate, report, and ultimately which software platform can support those expectations at scale.

The industry is increasingly bifurcating into two dominant engagement models. For third-party managers, understanding where an operator falls on this spectrum is essential to selecting technology that enables—not constrains—the relationship.

From a management company’s perspective, these models impose very different software requirements:

| Dimension | Full-Service Management (Operator Delegates Control) | Hybrid Support Model (Operator Retains Control) |

| Operational Control | The management firm has autonomy over daily operations, pricing, staffing, and enforcement. | The management firm supports execution, but the operator retains final decision-making authority. |

| Staffing Model | The manager hires, trains, and manages staff across the portfolio, requiring centralized workflows and labor optimization tools. | The operator hires staff; the manager provides systems, guardrails, and training frameworks. |

| Financial Oversight | The manager runs AP/AR, collections, and banking workflows, demanding GAAP-grade accounting and audit-ready reporting. | The operator maintains banking relationships; the manager needs transparent reporting and advisory visibility without full financial control. |

| Revenue Management | Pricing, ECRI execution, and promotions are fully automated and standardized by the manager. | Revenue strategy is co-managed; software must support scenario modeling, approvals, and visibility rather than unilateral execution. |

| Brand Structure | Assets are often re-flagged under the manager’s brand, requiring consistent brand-level reporting and portfolio segmentation. | Properties retain the operator’s brand, requiring clean brand separation, operator-specific dashboards, and flexible configuration. |

| Economic Structure | Higher management fees (typically 5–7% of gross revenue) justified by full operational delegation. | Lower percentage or flat-fee structures, where efficiency and transparency are critical to profitability. |

| Best Fit (Operator Profile) | Passive investors, institutional capital, and REIT-backed operators seeking a “set-it-and-forget-it” experience. | Active operators who want modern systems and expertise but retain strategic control. |

Why this matters for software selection:

A third-party management company supporting both full-service and hybrid operators cannot rely on rigid, one-size-fits-all systems. The platform must flex between full operational control and collaborative oversight—supporting delegated automation in one relationship and permission-based visibility in another. Software that assumes a single operating model forces managers to either over-control hybrid operators or under-deliver for full-service mandates.

In practice:

Management firms that scale successfully are those whose technology stack adapts to the operator’s governance model, not the other way around.

Beyond engagement models, third-party managers must evaluate software through the lens of portfolio complexity and long-term scalability. Several capabilities are non-negotiable.

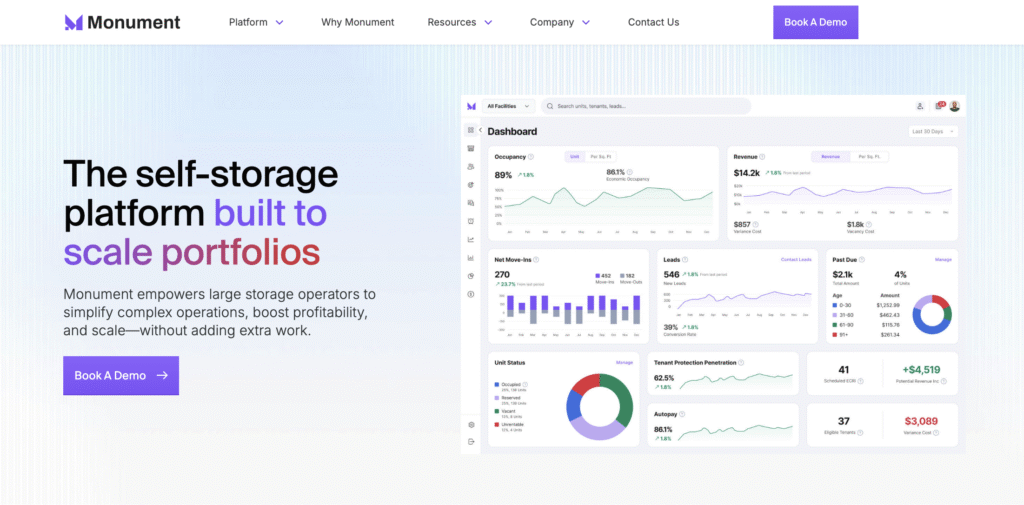

For third-party management firms, the software they choose is the foundation of their value proposition. These operators must deliver consistent NOI growth, operational discipline, and investor-grade reporting across portfolios they do not own. Monument was built specifically for this model—unlike legacy systems designed for single-site operators and later retrofitted for scale.

Two strong examples of this are Right Move Storage and The Storage Mall. Both organizations operate in environments where performance, standardization, and scalability are non-negotiable. They require a platform that can enforce consistent workflows, support sophisticated revenue management strategies, and provide portfolio-wide visibility without increasing overhead.

Monument serves as the technological backbone for operators like Right Move Storage and The Storage Mall, enabling them to centralize operations, automate revenue-critical processes, and deliver repeatable, high-yield outcomes for operators. By combining enterprise-grade automation, data-driven ECRI execution, and portfolio-level analytics, Monument allows third-party managers to scale their businesses while protecting margins and maintaining institutional standards across every asset they manage.

Legacy software often struggles with “portfolio-level” actions. Monument was purpose-built to solve this.

For third-party self-storage management companies, switching core systems can pose significant operational and financial risks. Monument was designed to remove that risk entirely by treating implementation and support as outcome-driven services, not ticket-based add-ons.

Efficiency is born from automation. Monument allows managers to script their operations.

Monument expands access to the sophisticated revenue tools previously reserved for public REITs.

For third-party management companies, the rental flow is a revenue engine. Monument focuses on materially improving conversion economics and average ticket value at the point of lease execution, without adding operational overhead.

Data is only useful if it is accessible.

The self-storage industry has moved beyond the phase of passive holding; it is now an active operational business where the quality of management dictates the return on investment. Whether you are a private operator looking to retire from daily operations or an institutional investor building a portfolio, partnering with a third-party self-storage management company is often the most direct path to maximizing NOI.

However, the partner you choose matters less than the tools they use. In an era of margin compression, you must align with managers who leverage enterprise-grade technology to automate operations, optimize revenue, and deliver transparent financial insights.

Next Steps:

If you are a third-party management firm or a multi-facility operator ready to upgrade your operational infrastructure, book a demo with Monument today.

Discover how our purpose-built platform can help you scale your portfolio, automate your workflows, and deliver REIT-level results for your assets.

Explore top self-storage software solutions with key features, comparisons, and tools for facility operations, marketing,...

Explore top facility management software systems for self-storage, including key features, benefits, and how these...

Maximize NOI with web-based self-storage software. Discover why modern portfolios require cloud-native management solutions for...